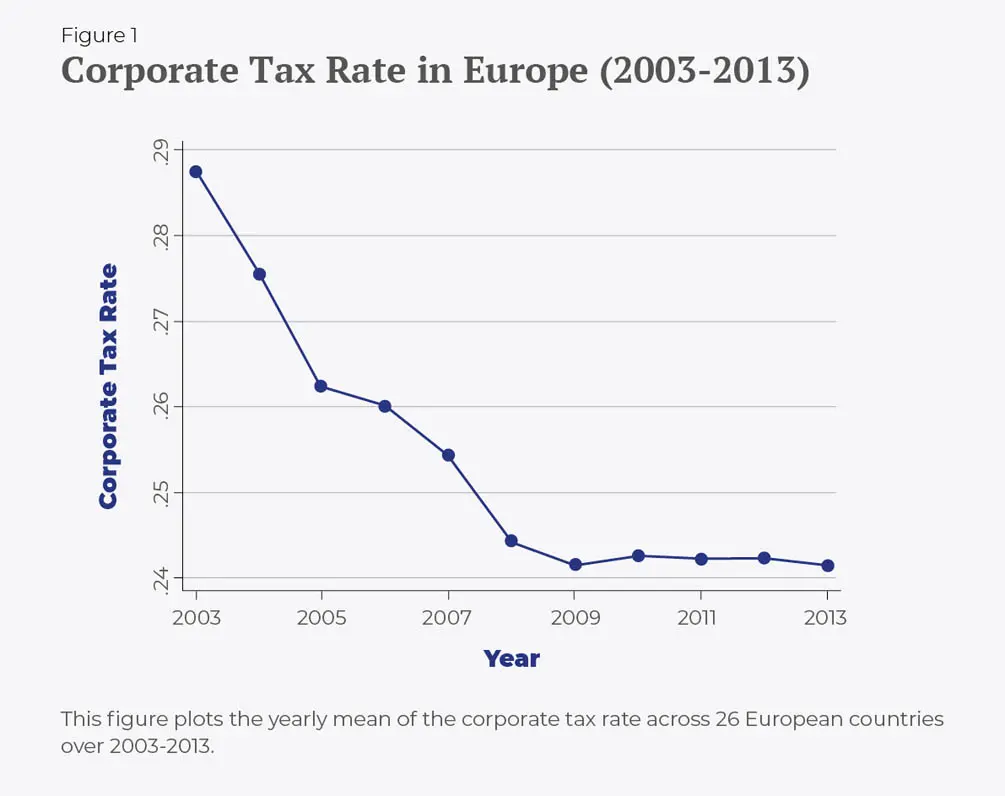

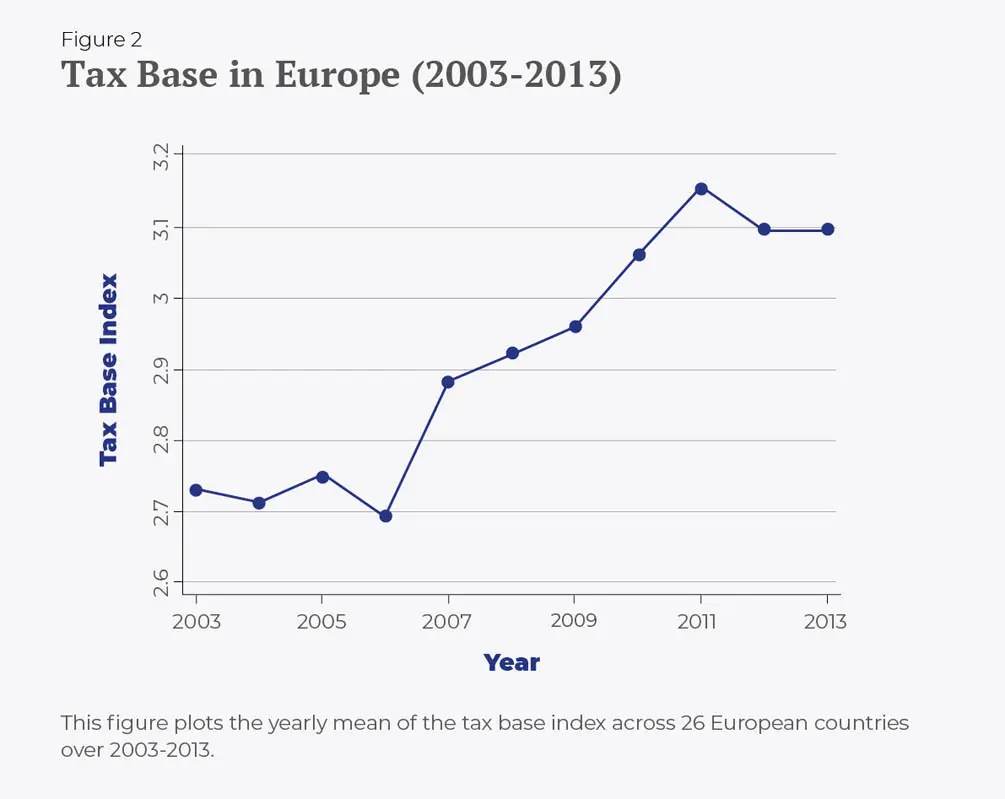

In the attempt to tackle the phenomenon, policymakers all over the world have put several countermeasures into law. In particular, European countries over the last decade have tightened anti-avoidance rules (i.e., laws curbing tax avoidance), lowered the Corporate Tax rate (see Figure 1), and broadened the tax base (i.e., increasing the portion of income subject to taxation, see Figure 2). Regulators in the European Union (EU) claim that these reforms have been effective in limiting tax avoidance However, despite the relevance of this claim, surprisingly, the empirical literature has so far neglected to test this conjecture.

In our paper “Corporate Tax Reforms and Tax-Motivated Profit Shifting: Evidence from the EU” (coauthored with Anna Alexander), we fill this gap and examine whether Corporate Tax reforms enacted across European countries over the past decade have constrained EU multinationals’ Profit Shifting. In this regard, the variety and heterogeneous implementation of BEPS countermeasures across EU countries and over time offer us a powerful setting to investigate whether Corporate Tax reforms have successfully constrained income shifting. Specifically, we identify how multinationals’ Profit Shifting responds to the changes to the bundle of specific tax base rules (i.e., transfer pricing documentation requirements, thin capitalization rules, tax consolidation rules, loss carryback and carryforward, accelerated tax depreciation allowances, and group tax relief). These rules jointly target Profit Shifting.

Our empirical approach proceeds in three steps. First, we estimate the tax rate sensitivity of multinationals’ Profit Shifting by conditioning our analyses on several changes in the tax base that occurred in Europe during 2003-2013. To estimate the joint tax rate and tax base effect on Profit Shifting, we combine the tax base elements into one overall index that measures the breadth of the tax base in a given country over time. In line with prior literature (Dischinger et al. 2014), we find that multinational companies shift profits into (or out of) their affiliates following a decrease (increase) in the tax rate of the host country (country where the subsidiary is located) or an increase (decrease) in the tax rate of the parent country (country where the headquarters are located). Importantly, we find that the income flowing between the host and parent countries is 25% lower when we account for policy changes that broaden the tax base (e.g., the introduction of transfer pricing documentation requirements and/or thin capitalization rules). In euro terms, we find that the income shifted into (or out of) an affiliate averages 1.3 million euros following a 10% change in the tax rate difference between the host and parent countries. However, this amount decreases by 0.24 million euros when the tax base is broader. Hence, the reforms in the EU that aimed at limiting income shifting have been successful.

Next, we examine whether the tax base-broadening reforms have a differential effect on inward Profit Shifting (i.e., shifting income into a foreign affiliate) and outward Profit Shifting (i.e., shifting income out of a foreign affiliate). Similar to previous studies (Beer and Loeprick 2015), we find that transfer pricing and thin capitalization rules prevent outward Profit Shifting. Interestingly, we also find that other tax base-broadening rules, such as restrictions on the deductibility of tax losses or on group tax relief, are equally relevant as they reduce the incentives for inward Profit Shifting.

Motivated by this evidence, we finally test whether Corporate Tax reforms have changed the trend in Profit Shifting in Europe over the past decade. The analyses point to a downward trend in Profit Shifting across European countries. Specifically, in the second half of our sample period (2007-2013), Profit Shifting decreased by more than 40%, and this decrease is even higher when we also account for the strength of tax enforcement. These findings suggest that broader tax bases and stronger tax enforcement have successfully constrained Profit Shifting over the years.

To conclude, our analysis provides a stark contrast to the conventional wisdom and prior evidence, which suggest that the tax avoidance (Dyreng et al. 2017) and income shifting (Grubert 2012; Klassen and Laplante 2012) of U.S. multinationals have increased over time. Our findings show that the income shifting of European multinationals—the key cross-border tax avoidance tool—has instead decreased over time, suggesting that single-country results from the United States cannot be extrapolated to Europe.

Finally, our results speak directly to the ongoing debate among OECD and EU countries about tackling income shifting and tax avoidance (OECD 2015; EU 2016). Although a coordinated agreement at the EU or the OECD levels has not been reached yet, countries can still tackle Profit Shifting on their own. As our results suggest, policymakers should continue enacting rules that broaden the tax base while strengthening tax enforcement. Taken together, our findings outline a path forward for countries to successfully curb Profit Shifting.

© IE Insights.