At the beginning of an economic crisis, policymakers try stimulative policies, usually through credit markets, as the first line of action until fiscal policy reacts. These credit policies can be classified in two broad groups: those that lower interest rates and others that provide subsidized funds to the financial sector so that it lends to households and firms. The goal is to stimulate credit markets to generate a virtuous cycle of higher economic activity through private investment and consumption. In the case of the 2008 Financial Crisis and, most recently, the COVID pandemic, the central banks and governments of many countries applied both types of credit policies at an unprecedented scale.

Although credit policies are widely used, the mechanism behind their operation actually remains relatively unknown. For example, there is little information available about which borrowers react more to credit policies. In a forthcoming paper in Management Science we tackle this question, with coauthors Sandeep Dahiya (from Georgetown University) and Lei Ge (from Renmin University), and show that the structure of executive compensation is an important determinant of the credit demand of the corporate sector. Our theory is as follows: credit stimuli generate opportunities to benefit from subsidized credit. This subsidized credit can be good for companies, though it does also entail some risk – and firms resort to giving their executives higher equity stakes in order to encourage them to take these risks, a benefit that is amplified as the executives reap a larger share of the higher firm value created by the subsidized borrowing.

Our empirical work exploits a unique setting that allows to separate credit supply from demand in order to test this theory. In 2008, to overcome the negative consequences of the global financial crisis, China implemented one of the largest credit stimuli in history, nearly 14% of the country’s 2008 GDP. During the pre-stimulus period, state-controlled banks in China originated most of the credit in the economy and these banks reacted strongly to the stimulus. “Beijing ordered banks to lend and they lent” and thus, it was the demand for credit, not supply, that determined what happened after the stimuli.

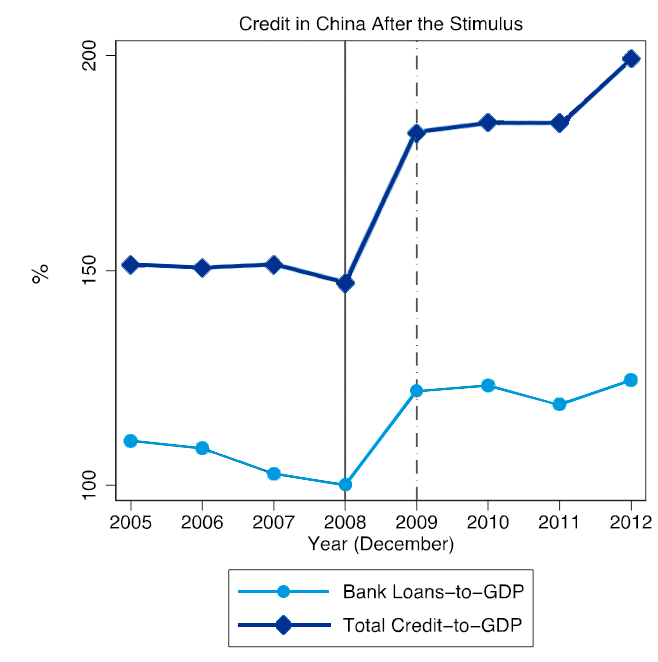

Figure 1: The Bank Loans-to-GDP is the ratio of the aggregate bank loans to GDP. The vertical solid line signals the end of 2008, which is when the credit stimulus was announced by the Chinese government. The vertical dashed line is the end of 2009, one year after the credit push. In 2009, the Bank Loans-to-GDP ratio shot up to almost 182% from 150% in 2008 and remained at this level for 2010. This represents an increase of more than 20% in a single year from a fairly stable baseline. The solid line plots the ratio of bank loans to GDP over the same period and shows that the bulk of the growth in credit was driven largely by growth in bank loans. This ratio grew from 100% in 2008 to 122% in 2009.

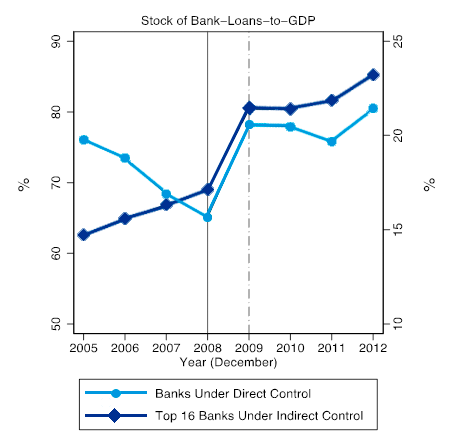

Figure 2: This figure shows that all banks followed the mandate of the Chinese government to try to lend more. It plots the ratio of bank loans to GDP for two types of banks in China. The solid line represents the total bank loans to GDP for all banks that are directly under state control. The dashed line plots the same ratio for 16 of the largest banks that are indirectly controlled by the government. Together, these two groups account for most of the bank lending in China. Comparing this ratio from the end of 2008 (when the credit shock occurred) to the end of 2010 shows that both groups increased their lending sharply and in a remarkably similar fashion.

This credit push by the Chinese government was largely unexpected and was therefore, it is safe to assume, not induced by the firms with higher managerial ownership, nor did the firms change the structure of management compensation in anticipation of the stimulus. This is important in order to correctly attribute the direction of causality. In other words, we can measure how the stimulus caused heterogeneous reactions across firms depending on the structure of their executive compensation absent of other factors that could drive such structures.

Following the capital structure literature, we excluded financial firms from our sample because they have higher leverage and are much more regulated than any other industry. Then, we compared the leverage in the pre- and post-stimulus periods exploiting cross-sectional differences in executive ownership levels across firms.

What we found is that, following the 2008 credit stimulus, firms with higher executive ownership levels (i.e., higher pay-for-performance sensitivity) borrowed more in order to expand their businesses relative to the firms with lower executive ownership levels. The results confirm that the structure of managerial compensation plays a significant role in influencing a firm’s reaction to a credit expansion. Those firms with managers that had higher equity incentives borrowed more because such borrowing was subsidized and worthy of the risk that it entailed. Equity incentives aligned managers with shareholders.

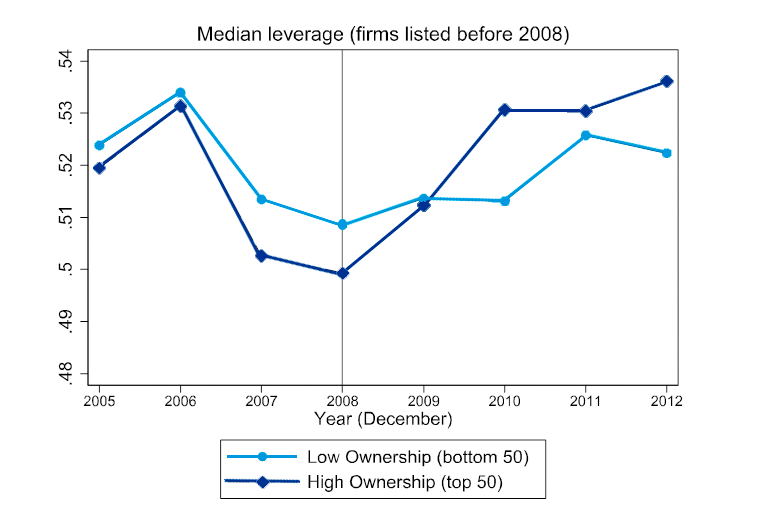

Figure 3: This figure plots the evolution of the leverage ratios for the “low executive ownership” and the “high executive ownership” firms during the period of 2005-2012. The solid black line represents the leverage ratio for the low ownership group while the dashed line represents the leverage ratio of the high ownership group. For the four-year period leading up to 2008, the leverage ratios for both groups appear to be following a similar trend. The leverage of low executive ownership firms is always larger than that of the high executive ownership firms. However, immediately after the 2008 credit stimulus, the leverage ratio of the high ownership group increased sharply and within two years it becomes larger than that of the low ownership group.

The ultimate goal for expansionary credit policies is to induce greater borrowing by households and corporations. However, as our research shows, when faced with an increased credit supply, not all firms respond in a similar manner. This may explain why credit policies produce different responses across countries. For example, it is possible that the credit policies in Japan, and to a certain extent in Europe, may not lead to significantly more borrowing by the corporate sector because executives do not have the levels of ownership as executives in Anglo Saxon countries. Greater managerial equity ownership creates conditions in which firms are more willing to increase leverage in response to a credit stimulus. Doing so will be good for society because economies will recover sooner from crises if credit policies are more effective.

© IE Insights.