Sustainable economic value creation is vital for a business to survive. To create value, the company must understand what economic advantages it has and accordingly make and implement decisions that ensure a level of profitability that exceeds the cost of the resources used. This underscores the relationship between strategy and economic value creation, however it is not an easy thing to measure in practice.

If we take that approach, we can conclude that discounted cash flow (DCF)—a traditional method of measuring economic value—does not fully quantify the value contributed by a strategic decision, since some of the value resulting from this decision goes unmeasured.

The economic value derived from DCF certainly has its limitations. For example, we must know what the actual flow is in terms of the amount and over time. The reality, however, shows that a possible future action on the project to be executed is not passive and sometimes involves a high value. This potential for action is called “operational flexibility.”

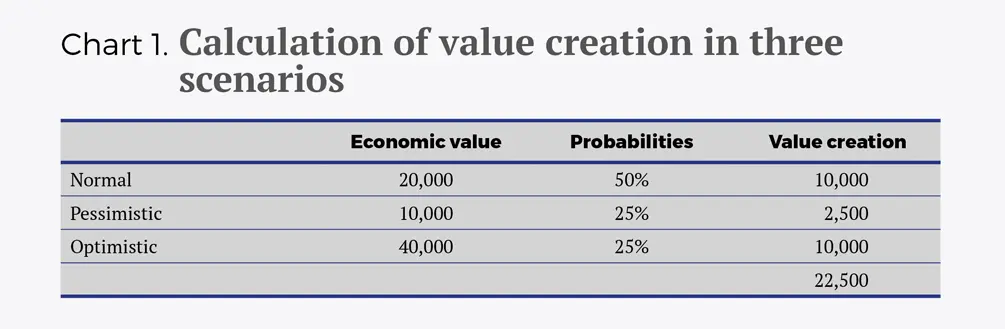

One way to incorporate the value of operational flexibility into the value obtained through DCF is to discount estimated cash flow based on the probabilities that a given scenario will materialize. In this case, the traditional DCF becomes dynamic since it factors in the probabilities of possible scenarios occurring. This is best illustrated with an example of investment analysis on a future project (see Chart 1), which reflects three possible scenarios of business development: Normal, optimistic and pessimistic. Every one of these would generate economic value, but they all have different probabilities, so the weighted average economic value would be 22,500 monetary units. In each case, we would need to analyze the value creation with the cash flows including the various actions that are taken based on the expected events (e.g., liquidating the business at a certain point in the pessimistic scenario or expanding it after reaching a particular level of cash generation).

When to Embrace Operational Flexibility

Given the uncertainty in some sectors, it is not always wise to be flexible at the operational level. Nevertheless, in order to take advantage of a market opportunity, any decision (strategic or otherwise) implies a series of risks when going after it decisively; those risks could entail disruptions such as changing the area of activity or technology of a business.

Therefore, along with taking DCF into account, the value measurement must be rounded out with other complementary methods. As such, it is crucial to evaluate not only the business decisions themselves, but also the model for quantifying their impact on value creation. Still, before running the numbers there are some key questions every organization must ask prior to undertaking any major project, regarding the real options of that project and whether they will have value in the future.

The act of betting on the classic method of discounted cash flow can underestimate the economic profitability of a project or particular investment.

Before Running the Numbers…

Before increasing the economic value of a decision, we must be sure that the option makes sense and has value. A real option when looking at the different possibilities of impact arises when changes in the environment are probable, since this implies, among other things, being able to delay the project, scrap it or, in the best-case scenario, expand it.

When considering the possible value, it is highly practical to break down the real options into two types:

- Exclusive or non-exclusive options. Obviously, a real option that is exclusive can bring more value, since there is an individual entitlement on the product or service that is being invested in.

- Explicit or implicit options. With the former, the company is guaranteed the aforementioned entitlement by means of a legal document.

Under this approach, for an option to have value it must be exclusive and implicit. So, for instance, the economic value of a project with high uncertainty, due to future technological development, will increase if there is an option to delay the project to see what happens with that development. Although it is true that, if the option to delay is not exclusive, i.e., if all competitors can do the same, that option will be of no value.

While it is good to use valuation models for real options in exclusive and explicit situations, it is also important to remember that these models have limitations, since they borrow their developments from options on financial futures. The main technical limitations arise with the analogous application of valid valuation techniques on financial assets and occur when the underlying asset is not traded in an organized public market or when the asset price does not follow a continuous process.

Using DCF in Conjunction with Other Valuation Techniques

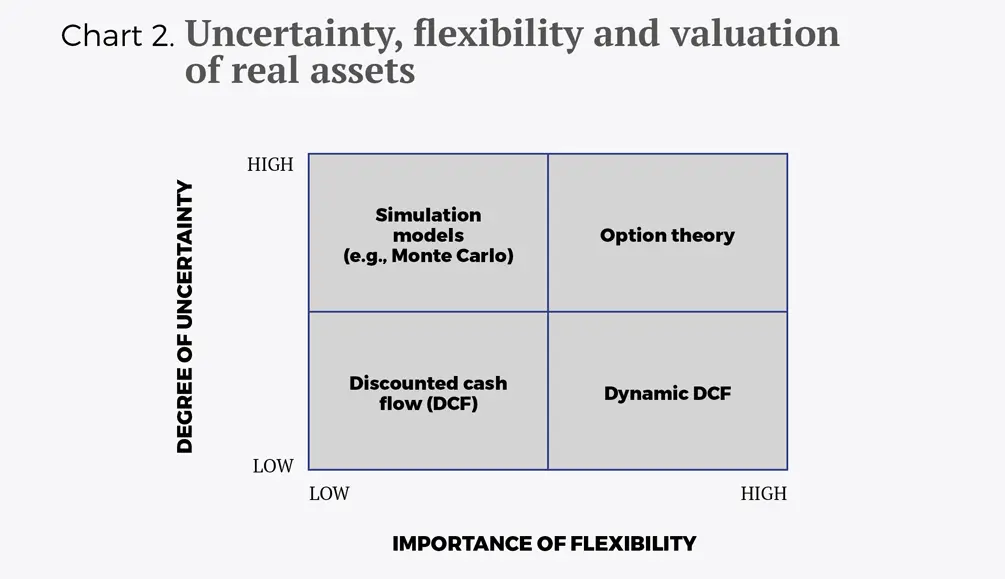

Ultimately, given that operational flexibility is a growing trend in the business world, the act of betting on the classic method of discounted cash flow can underestimate the economic profitability of a project or particular investment. So, despite certain limitations, we must consider adding other valuation techniques that include possible future scenarios, based on probabilities, such as dynamic DCF and option theory. Chart 2 shows the link between the degree of uncertainty, flexibility and valuation model for real assets.

© IE Insights.