- Home

- Hugo Chávez And His Legacy Of Inflation

Hugo Chávez and his legacy of inflation

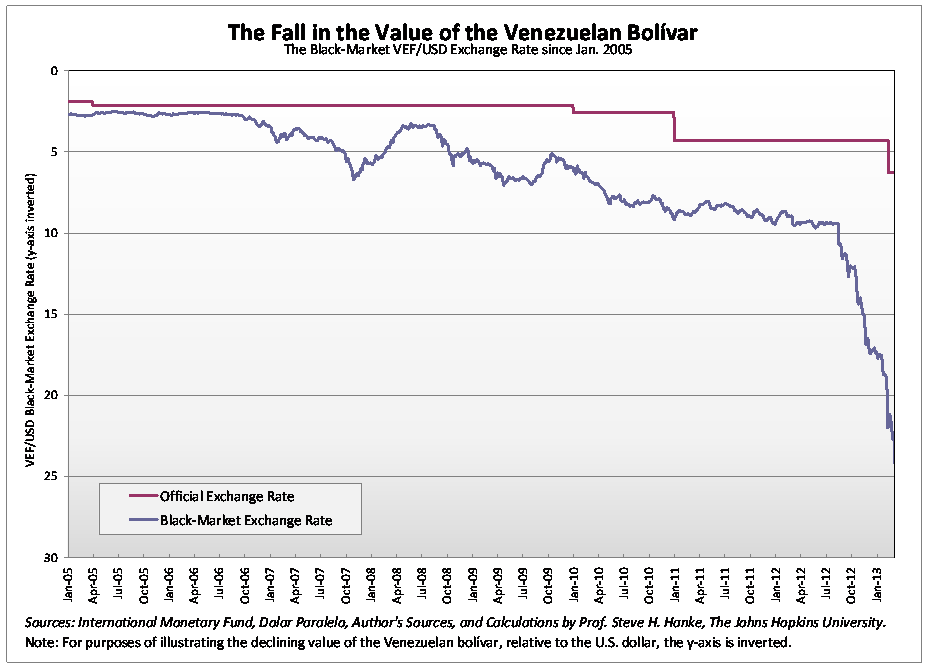

In February of 2013, the Hugo Chávez regime devalued its currency for the seventh time, bringing the fixed exchange rate from 4.3 to 6.3 bolivars to the dollar. The real market exchange rate, though, gives Venezuela’s currency a much lower valuation, closer to closer to a 25/1 rate.

{kind=link}

Now, with the socialist leader dead, his legacy will still hunt Venezuela in many ways. In terms of monetary policy, his regime managed to accumulate an inflation of 528% between 2003 and 2011. Such scandalous figure was followed by a 20% inflation rate in 2012. The outlook for 2013 is even worse, with estimates of a 30% rise in prices.

Food shortages are the norm, and price controls only make matters worse. The government has avoided popular unrest by extending subsidies and government programs, yet such scheme is simply not sustainable without historically high oil prices.

What should Venezuela do next in order to contain inflation and have a more stable monetary scenario? Ideally, the denationalization of money would be the best way to allow families and businesses to conduct their day-to-day operations in whichever currency they so desire.

Besides that best case scenario, two other options come to mind: on the one hand, imitating Ecuador’s experiment with dollarization; on the other hand, pegging the currency to a basket of U.S. dollars and oil prices. Both would be steps in the right direction, but they would have to be adopted along with three key reforms: end of price controls, reduction of public expenditures and economic liberalization.

Diego Sánchez de la Cruz is an analyst at Libertad Digital. His work on international economics has been published in different media outlets.