- Home

- We Are Law School

- News

- Mitchell Kane: “conceptual Understanding Allows Students To Quickly Master New Points Of Tax Law As They Arise In Practice”

Mitchell Kane: “Conceptual understanding allows students to quickly master new points of tax law as they arise in practice”

The Master in Global Taxation (LLM/MsL) includes a Global Experience Module in NYU School of Law. During this week, students gain a structural understanding of the main components of the U.S. tax system, which can be invaluable when interacting with U.S. tax professionals.

“Most global tax professionals will encounter the U.S. tax system at some point in their careers. The U.S. system is complex and includes many aspects that are unique and to which practitioners are unlikely to have encountered elsewhere”, said Gerald L. Wallace Professor of Taxation, Mitchell Kane, who shares his views on taxation in a global digital economy and how he prepares future tax professionals to tackle the new challenges.

What does your course cover?

The course covers a broad introduction to the fundamentals of U.S. international taxation from an inbound perspective (foreign persons conducting activity or investment in the U.S.) and from an outbound perspective (U.S. persons conducting activity or investment abroad). Specific doctrinal topics include the threshold requirements for when foreign persons are required to file a U.S. tax return, treatment of investments in U.S. securities and real estate, operation of the U.S. controlled foreign corporation rules, the U.S. foreign tax credit and participation exemption, and information exchange. The course also covers a range of more advanced planning topics, such as the formation and structure of funds seeking to invest in the U.S. and outbound IP migration structures. Key aspects of the U.S. tax reform of 2017 are incorporated throughout the materials.

“Tax professionals face the law of many jurisdictions in the course of a career. For this reason, I teach my students a blend of current doctrine and broader conceptual approaches to the law”

What is the correlation between tax reforms and economic growth?

The correlation between tax reforms and economic growth is a hotly disputed topic. Most tax reforms take too long to put in place to work as an immediate form of stimulus during the recession. Other policies, such as monetary policy, are typically preferred. However, in the long term, it can be expected that choices made through the tax system -- both with respect to overall burden and with respect to distribution of burden -- will have an important impact on growth patterns.

What are the main challenges for taxation and tax planning in the current global, digital economy? What is your view on taxing digital transactions?

The main challenge here is that taxable presence thresholds was defined for a bricks and mortar world and generally require concepts of physical presence. Thus, jurisdictions cannot reach foreign firms that are able to tap local markets without any physical presence. My personal view is that international tax norms will have to evolve in a way that allows market jurisdictions to reach a greater portion of the profits of foreign firms.

In your opinion, how should international double taxation evolve in order to deal with the pressures of globalization?

Over the course of the last century, we have moved from a state of affairs in which the chief concern internationally was excessive tax burden from overlapping taxing claims to a state of affairs where the concern is more about inadequate taxation. Globalization is part of this. The shift to an intangibles-based services economy is another part. To address this issue we will need to simultaneously bolster the principles of source-based tax and residence-based tax. We will also need to continue to have a more effective exchange of information across countries. Lastly, developing countries will have to be granted greater voice in the design of international tax policy.

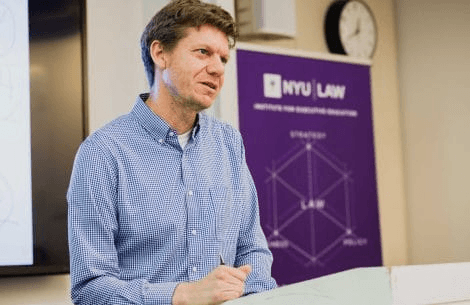

Professor Mitchell Kane teaching students of the Master in Global Tax during the NYU Experience Week in Greenwich Village Campus.

Professor Mitchell Kane teaching students of the Master in Global Tax during the NYU Experience Week in Greenwich Village Campus.What are the most important international tax developments?

In the U.S., the 2017 Tax Act included major changes to deal with both base erosion and undertaxation of intangibles-based profits of U.S. multinational firms. Much of the legislative text is filled with ambiguities.

The most important developments in the coming year(s) from the U.S. side will be the enactment of implementing regulations and clarification of the recently enacted reform.

How do you prepare students and future tax professionals to tackle all the current issues tax faces in a global, digital economy?

Tax law evolves rapidly and constantly. Tax professionals face the law of many jurisdictions in the course of a career. It is impossible to have current, comprehensive knowledge of all aspects of substantive law. For this reason, I teach my students a blend of current doctrine and broader conceptual approaches to the law. Conceptual understanding allows students to remain nimble and quickly master new points of law as they arise in practice.

How can taxes help combat climate change? What are your views on this?

Carbon taxes or permit trading markets help combat climate change by raising the price of greenhouse gasses to a point where price bears a closer relation to social cost. I believe greater reliance on these instruments is essential. The political hurdles in some jurisdictions, however, are very large. It is common in the United States to hear opponents of such instruments argue on the basis that carbon taxes will increase the cost of energy and slow economic growth. This, of course, is the whole point. Until there is a broader acknowledgment of this in the United States, it will be difficult to generate political consensus. Most of the rest of the world has shown a willingness to proceed without the U.S. But a properly functioning carbon tax must ultimately be a global instrument.

Why is this program valuable to global tax professionals?

Most global tax professionals will encounter the U.S. tax system at some point in their careers. The U.S. system is complex and includes many aspects that are unique to it and which practitioners are thus unlikely to have encountered elsewhere. This program gives tax professionals a structural understanding of the main components of the U.S. tax system which can be invaluable when interacting with U.S. tax professionals.